")

")

Dubai off-plan launches are built around one idea: urgency. “Launch price,” “early-bird,” “last units,” “today only.” The problem is that many buyers mistake a marketing label for a real discount. In practice, a launch price is only a deal if it is attractive versus the right comparables, after real costs, and with credible liquidity.

- The Trading Immo Rule

- What “Launch Price” Really Means (In Plain English)

- The 15-Minute Benchmark Framework (Fast and Practical)

- Step 1: Convert Everything to Price per sq.ft. (Non-Negotiable)

- Step 2: Benchmark Against 3 Comparable Buckets (Not One)

- Bucket A: Nearby resale (ready) comparables

- Bucket B: Competing off-plan launches nearby

- Bucket C: The “next-best substitute” area

- Step 3: Apply a Micro-Market Reality Check

- Step 4: Benchmark the Unit Type Liquidity (Rent + Resale)

- Step 5: Run a Fast Net Yield Sanity Check (Without Over-Engineering)

- Step 6: Identify Incentives That Hide Pricing Premiums

- Step 7: The “Stress Test” That Exposes Fake Deals

- A Simple “Deal Score” (Fast Decision)

- The Most Common Launch Pricing Mistakes

- Final Takeaway

This article gives you a fast benchmark method you can run in 15 minutes before paying any reservation fee. It won’t make you a valuer, but it will prevent the most common pricing mistake: buying an off-plan unit above fair value because the payment plan felt comfortable.

The Trading Immo Rule

A payment plan can improve cash management, but it can’t rescue an overpriced entry. In real estate, most “bad deals” start with one error: paying too much for the fundamentals you’re getting.

What “Launch Price” Really Means (In Plain English)

“Launch price” usually means one of three things:

-

The developer is pricing early units to build momentum (sometimes a real discount).

-

The developer is pricing high from day one but using urgency to accelerate sales.

-

The developer is bundling incentives (waived fees, flexible installments) to make the price feel lower without truly being lower.

Your job is to identify which one it is—quickly.

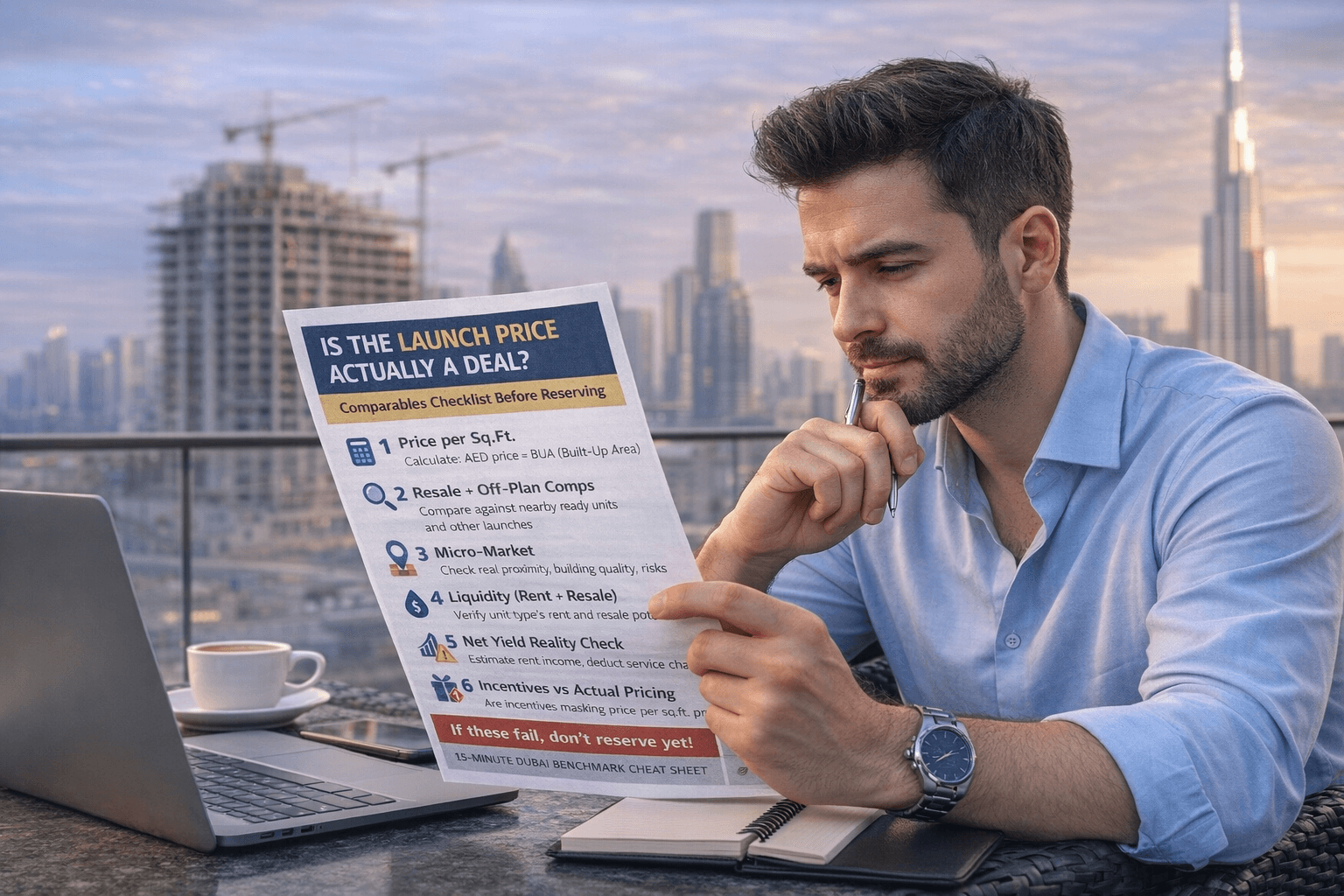

The 15-Minute Benchmark Framework (Fast and Practical)

You are going to benchmark using four filters:

-

Price per sq.ft. versus the right comps

-

Micro-market reality (not just the area name)

-

Net reality (service charges and running costs)

-

Exit liquidity (rent and resale)

If the launch price fails any one of these, it’s not a deal—it’s a dressed-up premium.

Step 1: Convert Everything to Price per sq.ft. (Non-Negotiable)

Get the unit’s:

-

Total price (AED)

-

Built-up area (BUA) in sq.ft.

Calculate: Price per sq.ft. = Total price ÷ BUA

Why this matters: you can’t benchmark without normalization. A “cheap” total price can be expensive per sq.ft. if the unit is small or inefficient.

Red flag: The agent avoids sharing BUA or uses unclear measurement.

Step 2: Benchmark Against 3 Comparable Buckets (Not One)

A real benchmark uses three buckets—because relying on only one reference set is how buyers get misled.

Bucket A: Nearby resale (ready) comparables

Look for 3–5 resale listings or recent transactions (where possible) in the same or neighboring micro-market for similar unit type (studio/1BR/2BR). This tells you what the market is paying today for a “ready” unit.

What you’re checking: is the launch price massively above resale reality with no justified premium?

Bucket B: Competing off-plan launches nearby

Compare to other off-plan projects delivering within a similar timeframe and targeting the same tenant/buyer profile.

What you’re checking: is this launch priced above alternatives that offer similar fundamentals?

Bucket C: The “next-best substitute” area

If your project is in an emerging area, compare it to a nearby area that already has proven demand. Buyers choose substitutes. Tenants choose substitutes. Your benchmark should too.

What you’re checking: is the premium logical, or are you paying proven-area pricing in a still-unproven location?

Trading Immo rule: If you can’t find at least 3 relevant comps, you don’t have enough clarity to reserve quickly.

Step 3: Apply a Micro-Market Reality Check

“Business Bay” is not one market. “JVC” is not one market. Buildings and sub-communities behave differently.

Check:

-

Distance to metro / key hubs (where relevant)

-

Immediate environment (roads, noise, construction zones)

-

Community quality and management reputation

-

View factors (open view vs blocked / future construction)

Two units in the same area can have a 15–30% valuation difference based on micro factors. If the launch price assumes “prime” micro positioning but the unit doesn’t have it, the “deal” is fake.

Step 4: Benchmark the Unit Type Liquidity (Rent + Resale)

A launch price can be “fair” on paper but still be a bad decision if the unit type is illiquid.

Ask:

-

Which unit type rents fastest in this micro-market?

-

Which unit type resells fastest when the market slows?

-

Is the layout efficient and livable, or is it awkward?

-

Is there oversupply risk for that size segment?

Rule: Liquidity beats discount. A slightly higher price on a liquid unit is often safer than a cheaper price on an illiquid unit.

Step 5: Run a Fast Net Yield Sanity Check (Without Over-Engineering)

You don’t need perfect rent numbers. You need a sanity range.

Estimate:

-

Conservative monthly rent range (based on comps)

-

Annual service charges estimate (or comparable buildings)

-

Basic management + maintenance reserve assumption

Then ask: does the “net reality” still make sense, or does the investment only look good on gross rent assumptions?

Red flag: The deal only works if rent is “best-case” and charges are ignored.

Step 6: Identify Incentives That Hide Pricing Premiums

Launches often include incentives:

-

waived DLD/registration items (sometimes partial)

-

“free” furniture packages

-

post-handover plans

-

discounted admin fees

These can be real value—but they are frequently used to hide inflated pricing.

Your test: if you remove the incentive value, is the price still competitive per sq.ft. versus comps? If not, you’re paying for the incentive through the unit price.

Step 7: The “Stress Test” That Exposes Fake Deals

Before reserving, apply three simple shocks:

-

Rent -10% from your assumption

-

Vacancy +1–2 months/year

-

Service charges +15%

If the investment becomes unattractive under mild stress, the launch price was not a deal—it was a marketing narrative.

A Simple “Deal Score” (Fast Decision)

Use this scorecard:

Likely a real deal if:

-

Price per sq.ft. is at or below strong comps (or justified by premium micro factors)

-

Unit type is liquid (rent + resale)

-

Net yield is reasonable after charges and conservative rent

-

Incentives are a bonus, not the reason the deal works

-

Exit plan is credible even in a slower cycle

Likely NOT a deal if:

-

Price is meaningfully above resale comps with no justification

-

The plan or incentive is the only “value”

-

The unit type is oversupplied or illiquid

-

Net numbers only work in best-case assumptions

The Most Common Launch Pricing Mistakes

-

Comparing only to other launches (ignoring resale reality)

-

Benchmarking by area name, not micro-market and building quality

-

Ignoring service charges (net yield collapse)

-

Buying the wrong unit type because it’s “cheaper”

-

Believing “today only” urgency instead of running a benchmark

Final Takeaway

A launch price is a deal only if it survives a fast benchmark:

-

normalized price per sq.ft.

-

relevant comps in three buckets

-

micro-market validation

-

liquidity check

-

net yield sanity check

-

incentive reality check

-

stress test

If one of these fails, don’t reserve quickly. Clarify first. That discipline is what separates investors from buyers reacting to marketing.

")

")