")

")

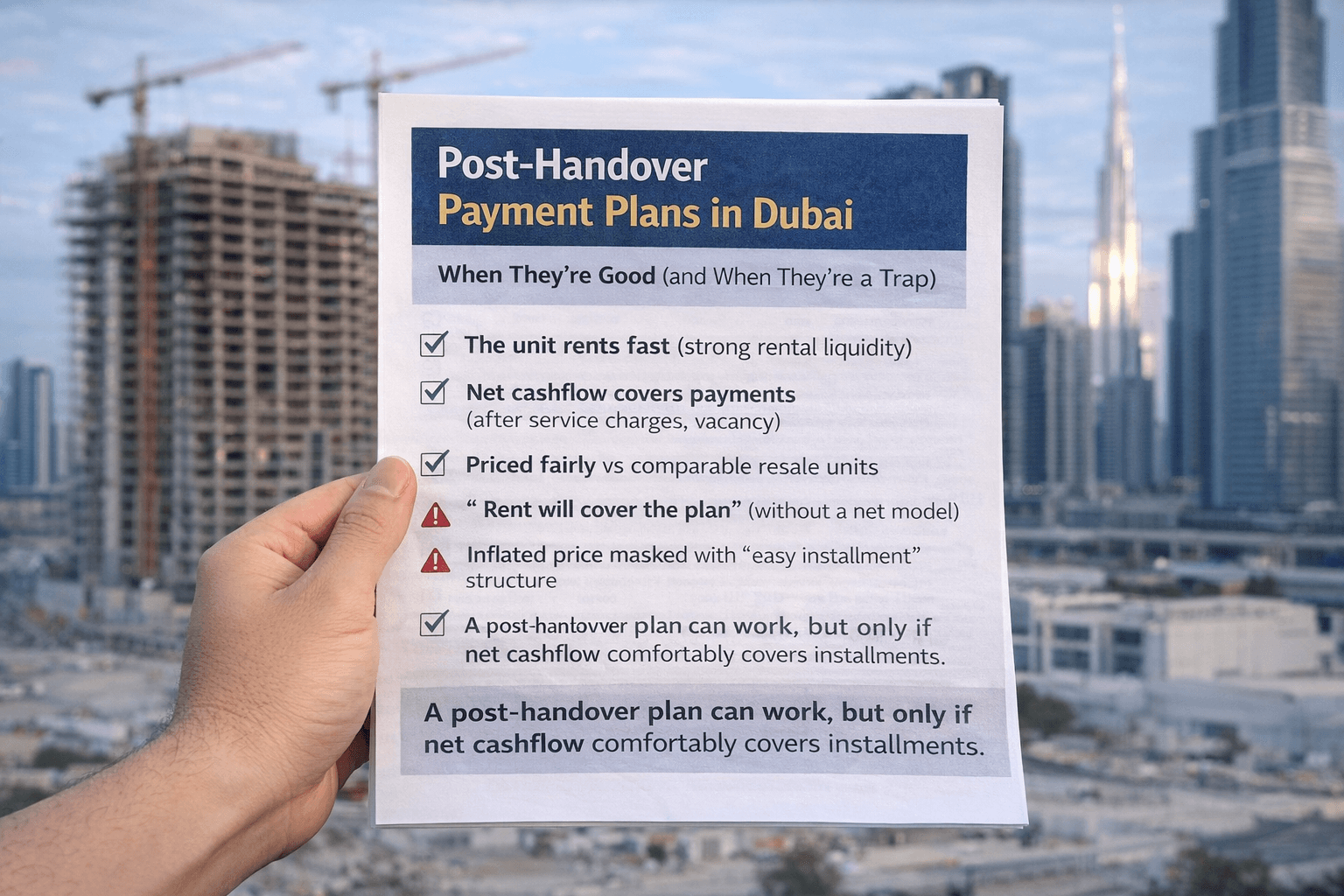

Post-handover payment plans are one of the most persuasive tools in Dubai off-plan marketing. The pitch sounds perfect: “Pay less now, get the keys, rent it out, and finish paying later.” Sometimes, that flexibility is genuinely useful. Often, it becomes a trap—because buyers confuse a convenient schedule with a strong investment.

- What “Post-Handover” Actually Means

- Why Post-Handover Plans Feel So Attractive

- The Trading Immo Rule

- When Post-Handover Plans Are Actually Good

- 1) Rental liquidity is strong (the unit rents fast at market price)

- 2) Net cashflow comfortably covers the post-handover installment

- 3) Service charges are reasonable relative to rent

- 4) You have a buffer for the first 60–90 days after handover

- 5) The entry price is still fair versus comparables

- When Post-Handover Plans Become a Trap

- Trap 1: “Rent will pay the plan” without a net model

- Trap 2: High service charges masked by “easy installments”

- Trap 3: Weak demand for that unit type (especially oversupplied stock)

- Trap 4: Illiquidity on resale (you can’t exit when you need to)

- Trap 5: The plan is used to hide inflated pricing

- The 6 Numbers You Must Check Before Reserving

- A Simple Decision Test (Fast)

- Practical Example Logic (How to Think Like an Investor)

- Final Takeaway

This article explains, in a practical investor framework, when post-handover plans work, when they don’t, and what you must calculate before paying any reservation fee.

What “Post-Handover” Actually Means

A post-handover plan simply means that a portion of the unit price is paid after you receive the keys. Common structures include:

-

A standard split (e.g., 60/40 or 70/30) where part of the “40” or “30” is spread over 1–5 years post-handover

-

A larger post-handover portion marketed as “easy installments”

-

Plans positioned as “rent will cover it,” typically linked to smaller recurring payments

Important nuance: post-handover does not mean low risk. It means your payment timeline extends into the period when the property can, in theory, generate income. But income is never guaranteed, and costs start immediately at handover.

Why Post-Handover Plans Feel So Attractive

Post-handover plans reduce psychological friction for buyers, especially non-residents:

-

Lower immediate cash pressure

-

A feeling of affordability (“I don’t need to pay everything at handover”)

-

A belief that rent will naturally cover payments

-

A sense of safety compared to a large one-time handover payment

The marketing works because it focuses attention on monthly installments rather than on the two questions that matter most: “Am I overpaying?” and “Will the net numbers hold under stress?”

The Trading Immo Rule

A payment plan is not the deal. It’s the payment schedule for the deal. A flexible plan cannot fix weak fundamentals, inflated pricing, high service charges, or an illiquid unit type. If the investment is weak, the plan just delays the moment you realize it.

When Post-Handover Plans Are Actually Good

A post-handover plan can be a legitimate advantage when all of the conditions below are met.

1) Rental liquidity is strong (the unit rents fast at market price)

Post-handover only works smoothly if the unit can be rented quickly after handover. That depends on:

-

proven tenant demand in the area

-

a unit type that matches that demand (often 1BR in many markets, but not always)

-

a livable layout (not just a small BUA with awkward space)

-

a building/community that is attractive at handover

If your unit sits empty for 2–3 months, your “flexibility” becomes immediate cash pressure.

2) Net cashflow comfortably covers the post-handover installment

This is where most buyers get misled: they evaluate gross rent, not net income.

Your net model must include:

-

service charges (annual, but real)

-

property management fees (common for non-residents)

-

maintenance reserve

-

vacancy assumptions (even in good markets)

-

leasing costs and minor setup expenses

If your post-handover installment is close to your net monthly income, the plan is fragile. One vacancy period, one rent reduction, or one service-charge increase can turn the deal negative.

3) Service charges are reasonable relative to rent

Service charges are the silent killer of post-handover plans. Two buildings can have the same gross rent, but one can produce significantly lower net cashflow because charges are higher.

If charges are high, you need exceptional rental demand and a premium product to maintain net performance. Without that, the plan becomes a burden.

4) You have a buffer for the first 60–90 days after handover

Even in the best scenario, handover-to-first-rent usually takes time:

-

snagging/defect fixes

-

DEWA setup and utilities

-

furnishing and staging (if applicable)

-

listing, viewings, tenant screening

-

contract and move-in timeline

A post-handover plan is safest if you can handle 1–3 months of expenses without stress. If you “need” rent immediately, you are over-leveraging your assumptions.

5) The entry price is still fair versus comparables

This is the most important condition. Many post-handover plans are attached to pricing premiums. You feel like you’re gaining flexibility, but you’re actually paying for it in the purchase price.

If you pay 10–20% above fair market value to access a post-handover plan, you may lose more in capital value and exit liquidity than you gain in payment comfort.

A good plan on a bad price is still a bad deal.

When Post-Handover Plans Become a Trap

Here are the most common situations where post-handover turns into a costly mistake.

Trap 1: “Rent will pay the plan” without a net model

If the sales pitch uses rent to justify the plan but ignores:

-

service charges

-

vacancy

-

management fees

-

maintenance

-

leasing/turnover costs

…then it’s marketing, not analysis.

Your rent is not profit. Your net cashflow is what matters.

Trap 2: High service charges masked by “easy installments”

Premium communities and branded buildings often carry higher service charges. That may be acceptable if the unit is highly rentable and liquid. But if rent growth does not keep up with charges, your net performance compresses and the plan becomes heavy.

Trap 3: Weak demand for that unit type (especially oversupplied stock)

Post-handover plans are dangerous when you buy:

-

a unit type that is heavily oversupplied in the area

-

a layout that is hard to live in (hard to rent, hard to resell)

-

a building competing with many similar handovers at the same time

If you can’t rent quickly, you end up paying installments without income.

Trap 4: Illiquidity on resale (you can’t exit when you need to)

Many buyers assume they can exit easily “if needed.” But resale liquidity is not guaranteed, particularly if:

-

many similar units are listed

-

the market cools at handover

-

you entered at a premium price

-

the building’s reputation is weak

In a slow market, the ability to resell quickly becomes the difference between flexibility and stress.

Trap 5: The plan is used to hide inflated pricing

This is the classic trap: the developer uses post-handover structure to justify a higher price, knowing buyers focus on monthly installments. You feel protected, but you are paying the flexibility upfront.

If the plan is the main reason the deal looks attractive, you need to benchmark the price again—more aggressively.

The 6 Numbers You Must Check Before Reserving

If you want a simple investor filter, use these six numbers:

-

Total price vs comparables (is the entry price disciplined?)

-

% due before handover (how much capital is locked without income?)

-

% due post-handover + duration (what is the real monthly burden?)

-

Conservative expected rent (not “best case”)

-

Service charges estimate (and what is “high” in that micro-market)

-

Net monthly cashflow vs installment (must cover with margin)

Core rule: if your realistic net monthly cashflow does not cover the post-handover installment comfortably, the plan is not working for you—it’s working against you.

A Simple Decision Test (Fast)

A post-handover plan is generally acceptable when:

-

the unit will rent fast (proven rental liquidity)

-

you have a cash buffer for handover and initial months

-

net cashflow covers installments with margin

-

pricing is not inflated versus comparables

-

resale liquidity is credible in a slower market

If any one of these conditions fails, treat the plan as a trap until proven otherwise.

Practical Example Logic (How to Think Like an Investor)

Don’t ask “Can I afford the installment?” Ask:

-

Can I afford it with rent assumed at a conservative level?

-

Can I afford it if it takes 2 months to rent?

-

Can I afford it if service charges increase?

-

Can I afford it if the market is slower at handover and rent is negotiated down?

If you need perfect conditions for the plan to work, it’s not a plan—it’s a gamble.

Final Takeaway

Post-handover plans are not automatically good or bad. They are a tool. They are good when the underlying asset is liquid, service charges are manageable, net cashflow covers the schedule, and the entry price is fair. They become a trap when they mask inflated pricing, rely on optimistic occupancy assumptions, or attach you to an illiquid unit type.

")

")